FROM OUR BLOG

FROM OUR BLOG

FROM OUR BLOG

What is SWP ? | Fixed Income from MF

Jun 21, 2025

Imagine you have a piggy bank where, whenever you put money in, it increases that amount slightly. So, if you put ₹1000 into the piggy bank, as soon as the money goes in, it becomes ₹1100. The piggy bank itself adds ₹100—so in a way, it’s a magical piggy bank.

Now, let’s say you’ve been putting money into this magical piggy bank for the past 10 years—sometimes ₹1000, sometimes ₹2000, sometimes ₹5000. Over 10 years, you have deposited ₹1 lakh in total. And because this piggy bank is magical, that ₹1 lakh has now grown to ₹1.5 lakh—meaning the piggy bank has added ₹50,000 on its own.

Now, you tell the piggy bank, "I don’t want to spend this ₹1.5 lakh all at once. Instead, I want to withdraw ₹1000 per month from it."

The piggy bank then tells you, "I will give you ₹1000 every month for the next 15 years, and even after 10 years, I will grow your ₹1.5 lakh into ₹3 lakh."

You invested money into a magical piggy bank for 10 years.

Then, after 10 years, you started withdrawing a fixed amount from it every month—just like a monthly income.

For the next 15 years, you withdraw a fixed amount every month, but despite that, your initial amount of ₹1.5 lakh (in this case) doesn’t deplete—it actually grows. This is a Systematic Withdrawal Plan (SWP).

Benefits of SWP

SWP (Systematic Withdrawal Plan) is highly beneficial Plans , Here are the key benefits of an SWP plan:

1. Flexibility

Invest and withdraw as per your financial needs.

No fixed tenure—start, stop, or modify the plan anytime.

2. Regular Monthly Income

Ensures a steady cash flow, making it ideal for retirees or those seeking passive income.

Helps manage expenses without worrying about market fluctuations.

3. Capital Growth & Appreciation

If the withdrawal rate is lower than the fund returns, your invested capital continues to grow.

Over time, your corpus can increase instead of depleting.

4. Tax Efficiency

Unlike Fixed Deposits, only the withdrawn amount is taxed, not the entire corpus.

LTCG (Long-Term Capital Gains) tax benefits apply, making it more tax-friendly.

No TDS (Tax Deducted at Source) on withdrawals.

5. No Lock-in Period

Unlike fixed deposits or pension plans, SWP has no mandatory lock-in.

You can access your money anytime without penalties.

How Does SWP Work in Mutual Funds? (With Real Life Example of SWP )

Let’s look at a real-life example to give you more context on how SWP works—this example will also help you understand the numbers better.

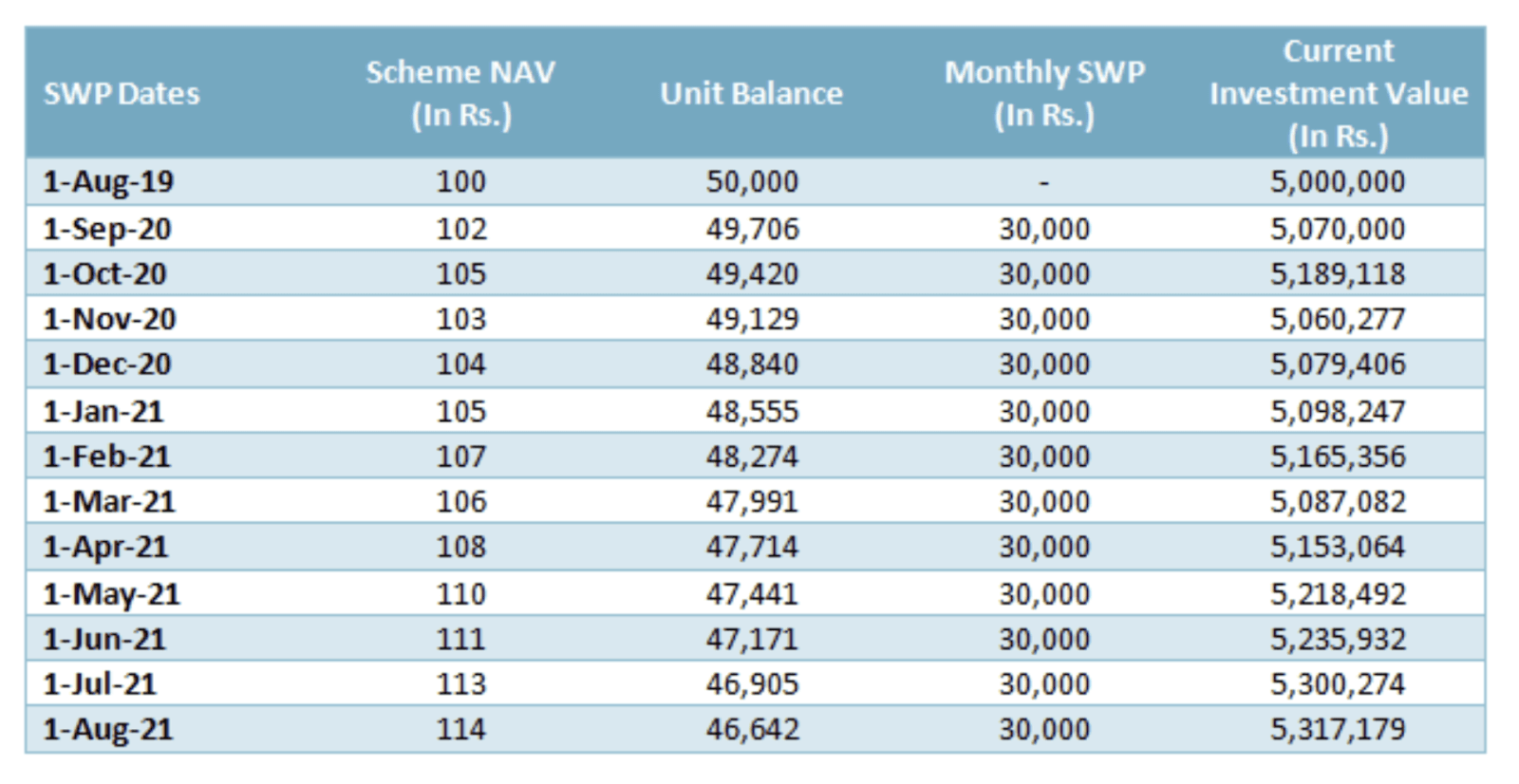

This is a real example of a Balanced Advantage Fund. I have removed the fund’s name to avoid any confusion. Just focus on the numbers.

The last column shows the Current Investment Value, which is similar to how our piggy bank had grown to ₹1.5 lakh after 10 years. In this case, the amount is ₹50 lakh.

The total investment value is ₹50 lakh, and the total number of units is 50,000. Just like listed companies have shares, mutual funds have units. And just like shares have a share price, mutual funds have something called NAV (Net Asset Value).

In this case, there are 50,000 units, and each unit is priced at ₹100—meaning the NAV is ₹100.

The total investment value is calculated as

Total Number of Units × Price of 1 Unit (NAV) = 50,000 × 100 = ₹50 lakh.

Now, you start withdrawing ₹30,000 per month from this amount. At the same time, the fund also generates returns every month. Here, we have shown the actual market returns of this fund.

In the first month, when you withdrew ₹30,000, the NAV increased from ₹100 to ₹102—which means the fund grew by 2% that month.

So, to withdraw ₹30,000, you had to redeem approximately 294 units (Screen will show: 30,000 / 102 = 294 units).

After this withdrawal, you are left with 49,706 units.

This means that after withdrawing ₹30,000 in the first month, your number of units decreased slightly, but the price of each unit increased from ₹100 to ₹102.

In the second month, when you withdrew another ₹30,000, the NAV increased from ₹102 to ₹105.

So, you had to redeem approximately 286 units (30,000 / 105 = 286 units) .After this withdrawal, you are left with 49,420 units.

Now, you don’t need to manually calculate how many units to withdraw or how many are left—this all happens automatically in the background. I am only showing this to help you understand the process.

You continue withdrawing ₹30,000 per month like this.

Now, focus on the last row, which represents the scenario after one year:

Your total units decreased from 50,000 to 46,642.

The NAV increased from ₹100 to ₹114.

Your total investment value, which is calculated as Total Units × NAV, increased from ₹50 lakh to ₹53.17 lakh.

So, think about this deeply..

At the beginning of the year, your portfolio was worth ₹50 lakh.

You withdrew ₹30,000 every month throughout the year.

Yet, at the end of the year, your portfolio grew from ₹50 lakh to ₹53.17 lakh!

Amazing, right? This is SWP—or Systematic Withdrawal Plan.

One more thing—I haven't mentioned taxation in this discussion to keep things simple.

However, SWP is subject to LTCG (Long-Term Capital Gains) tax.

But don’t worry about it for now—by the time you start thinking about taxes, you’ll already understand the entire SWP strategy.

How Much Should You Invest in SWP

Now, let’s see how much you need to invest,

As we saw in our previous examples, to withdraw a monthly income, you first need a large corpus. In our last example, that corpus was ₹50 lakh.

If you already have this amount today, that’s great!

If not, then your first step is to build this corpus—and you can do that through SIP (Systematic Investment Plan).

How much corpus do you need?

This depends on:

How much monthly income you want to withdraw.

After how many years you want to start withdrawing.

How to Grow your Corpus if you have Zero Corpus ?

Suppose you want to withdraw ₹50,000 per month 20 years later but right now, you have zero corpus.

To achieve this, you can start investing ₹10,000 per month in SIP for the next 20 years With an average return of 12%, after 20 years, your corpus will grow to ₹1 crore.

Now, 20 years later, you can set up an SWP of ₹50,000 per month from your ₹1 crore corpus.

This means you will withdraw ₹6 lakh per year, which is 6% of your ₹1 crore corpus.

Meanwhile, your ₹1 crore portfolio will continue to grow at an average of 8-10% per year.

Since you are withdrawing only 6%, your entire monthly income will be covered by the returns alone—you won’t even need to touch your ₹1 crore corpus.

In fact, even after withdrawing 6% annually, your corpus will still grow by 2-3% every year.

Investment Amount Based on Your Goal

If you want ₹1 lakh per month after 20 years, you should start investing ₹20,000 per month now.

If you want ₹1.5 lakh per month, you should start investing ₹30,000 per month, and so on.

How to set up SWP?

Now, one question remains—how do you actually set up this system?

Do you need to fill out any extra forms or make some settings in the app?

The answer is no extra steps are needed.

The app you use for SIPs (or plan to use) already has an SWP option for most mutual funds—you just need to select it.

I know for a fact that top apps like Zerodha and Groww have this option.

I can't say with 100% certainty about other apps, but most of them should have it.

Setting up SWP is even easier than setting up SIP—you just need to go and select the option!

Who Should Invest in an SWP Plan?

The Systematic Withdrawal Plan (SWP) is a great investment option for individuals who need a regular cash flow while ensuring their capital keeps growing. Here’s who can benefit the most from it:

1. Retirees Looking for a Stable Income

Ideal for those who no longer have a fixed salary but need a steady monthly income.

Helps cover daily expenses without depleting savings.

2. Individuals with Financial Dependents

Suitable for people who have family members relying on them, such as children, elderly parents, or spouses.

Ensures a continuous flow of income to manage household expenses.

3. Investors Seeking Passive Income

Perfect for those who want to create an additional income stream while keeping their investments intact.

A great way to supplement earnings without actively managing investments.

4. Individuals Who Want to Beat Inflation

Bank FDs and traditional savings often fail to keep up with inflation.

SWP provides market-linked returns, helping your wealth grow over time.

5. People Who Want Tax-Efficient Withdrawals

Unlike fixed deposits, SWP offers lower tax liability due to long-term capital gains tax benefits.

No TDS (Tax Deducted at Source) on withdrawals.

6. Those Who Prefer Low-Risk, Disciplined Investing

SWP ensures regular withdrawals without panic-selling in volatile markets.

Eliminates the need to time the market, making it a stress-free investment option.

Best SWP Calculator

SWP stands for systematic withdrawal plan. If you invest a lump-sum amount in a mutual fund and you want to withdraw a certain amount regularly, then you can do the same with the help of SWP. And to calculate the total withdrawable amount, the final amount, and the amount invested, we use the SWP calculator.

Link - https://bekifaayati.co/pages/swp-calculator/

Factors to Consider Before Investing in SWP Funds

Strong Track Record – Choose funds with a consistent performance history for stable returns.

Low Fees – Opt for funds with a reasonable expense ratio to maximize profits.

Risk-Return Balance – Understand the risk level of the fund and match it with your financial goals.

Fund Type & Asset Allocation – Pick between equity, debt, or hybrid funds based on your risk appetite and withdrawal timeline.

Tax Efficiency – Be aware of capital gains tax on withdrawals to optimize returns.

Conclusion

SWP is a simple yet effective way to create a regular income stream while keeping your money invested for growth. It works well for retirees, individuals with dependents, or anyone looking for financial stability without relying on market timing.

The key to making the most of SWP is choosing the right fund, understanding withdrawal rates, and staying consistent with your investment approach. With proper planning, SWP can help you maintain cash flow, grow your wealth, and secure your financial future.

Imagine you have a piggy bank where, whenever you put money in, it increases that amount slightly. So, if you put ₹1000 into the piggy bank, as soon as the money goes in, it becomes ₹1100. The piggy bank itself adds ₹100—so in a way, it’s a magical piggy bank.

Now, let’s say you’ve been putting money into this magical piggy bank for the past 10 years—sometimes ₹1000, sometimes ₹2000, sometimes ₹5000. Over 10 years, you have deposited ₹1 lakh in total. And because this piggy bank is magical, that ₹1 lakh has now grown to ₹1.5 lakh—meaning the piggy bank has added ₹50,000 on its own.

Now, you tell the piggy bank, "I don’t want to spend this ₹1.5 lakh all at once. Instead, I want to withdraw ₹1000 per month from it."

The piggy bank then tells you, "I will give you ₹1000 every month for the next 15 years, and even after 10 years, I will grow your ₹1.5 lakh into ₹3 lakh."

You invested money into a magical piggy bank for 10 years.

Then, after 10 years, you started withdrawing a fixed amount from it every month—just like a monthly income.

For the next 15 years, you withdraw a fixed amount every month, but despite that, your initial amount of ₹1.5 lakh (in this case) doesn’t deplete—it actually grows. This is a Systematic Withdrawal Plan (SWP).

Benefits of SWP

SWP (Systematic Withdrawal Plan) is highly beneficial Plans , Here are the key benefits of an SWP plan:

1. Flexibility

Invest and withdraw as per your financial needs.

No fixed tenure—start, stop, or modify the plan anytime.

2. Regular Monthly Income

Ensures a steady cash flow, making it ideal for retirees or those seeking passive income.

Helps manage expenses without worrying about market fluctuations.

3. Capital Growth & Appreciation

If the withdrawal rate is lower than the fund returns, your invested capital continues to grow.

Over time, your corpus can increase instead of depleting.

4. Tax Efficiency

Unlike Fixed Deposits, only the withdrawn amount is taxed, not the entire corpus.

LTCG (Long-Term Capital Gains) tax benefits apply, making it more tax-friendly.

No TDS (Tax Deducted at Source) on withdrawals.

5. No Lock-in Period

Unlike fixed deposits or pension plans, SWP has no mandatory lock-in.

You can access your money anytime without penalties.

How Does SWP Work in Mutual Funds? (With Real Life Example of SWP )

Let’s look at a real-life example to give you more context on how SWP works—this example will also help you understand the numbers better.

This is a real example of a Balanced Advantage Fund. I have removed the fund’s name to avoid any confusion. Just focus on the numbers.

The last column shows the Current Investment Value, which is similar to how our piggy bank had grown to ₹1.5 lakh after 10 years. In this case, the amount is ₹50 lakh.

The total investment value is ₹50 lakh, and the total number of units is 50,000. Just like listed companies have shares, mutual funds have units. And just like shares have a share price, mutual funds have something called NAV (Net Asset Value).

In this case, there are 50,000 units, and each unit is priced at ₹100—meaning the NAV is ₹100.

The total investment value is calculated as

Total Number of Units × Price of 1 Unit (NAV) = 50,000 × 100 = ₹50 lakh.

Now, you start withdrawing ₹30,000 per month from this amount. At the same time, the fund also generates returns every month. Here, we have shown the actual market returns of this fund.

In the first month, when you withdrew ₹30,000, the NAV increased from ₹100 to ₹102—which means the fund grew by 2% that month.

So, to withdraw ₹30,000, you had to redeem approximately 294 units (Screen will show: 30,000 / 102 = 294 units).

After this withdrawal, you are left with 49,706 units.

This means that after withdrawing ₹30,000 in the first month, your number of units decreased slightly, but the price of each unit increased from ₹100 to ₹102.

In the second month, when you withdrew another ₹30,000, the NAV increased from ₹102 to ₹105.

So, you had to redeem approximately 286 units (30,000 / 105 = 286 units) .After this withdrawal, you are left with 49,420 units.

Now, you don’t need to manually calculate how many units to withdraw or how many are left—this all happens automatically in the background. I am only showing this to help you understand the process.

You continue withdrawing ₹30,000 per month like this.

Now, focus on the last row, which represents the scenario after one year:

Your total units decreased from 50,000 to 46,642.

The NAV increased from ₹100 to ₹114.

Your total investment value, which is calculated as Total Units × NAV, increased from ₹50 lakh to ₹53.17 lakh.

So, think about this deeply..

At the beginning of the year, your portfolio was worth ₹50 lakh.

You withdrew ₹30,000 every month throughout the year.

Yet, at the end of the year, your portfolio grew from ₹50 lakh to ₹53.17 lakh!

Amazing, right? This is SWP—or Systematic Withdrawal Plan.

One more thing—I haven't mentioned taxation in this discussion to keep things simple.

However, SWP is subject to LTCG (Long-Term Capital Gains) tax.

But don’t worry about it for now—by the time you start thinking about taxes, you’ll already understand the entire SWP strategy.

How Much Should You Invest in SWP

Now, let’s see how much you need to invest,

As we saw in our previous examples, to withdraw a monthly income, you first need a large corpus. In our last example, that corpus was ₹50 lakh.

If you already have this amount today, that’s great!

If not, then your first step is to build this corpus—and you can do that through SIP (Systematic Investment Plan).

How much corpus do you need?

This depends on:

How much monthly income you want to withdraw.

After how many years you want to start withdrawing.

How to Grow your Corpus if you have Zero Corpus ?

Suppose you want to withdraw ₹50,000 per month 20 years later but right now, you have zero corpus.

To achieve this, you can start investing ₹10,000 per month in SIP for the next 20 years With an average return of 12%, after 20 years, your corpus will grow to ₹1 crore.

Now, 20 years later, you can set up an SWP of ₹50,000 per month from your ₹1 crore corpus.

This means you will withdraw ₹6 lakh per year, which is 6% of your ₹1 crore corpus.

Meanwhile, your ₹1 crore portfolio will continue to grow at an average of 8-10% per year.

Since you are withdrawing only 6%, your entire monthly income will be covered by the returns alone—you won’t even need to touch your ₹1 crore corpus.

In fact, even after withdrawing 6% annually, your corpus will still grow by 2-3% every year.

Investment Amount Based on Your Goal

If you want ₹1 lakh per month after 20 years, you should start investing ₹20,000 per month now.

If you want ₹1.5 lakh per month, you should start investing ₹30,000 per month, and so on.

How to set up SWP?

Now, one question remains—how do you actually set up this system?

Do you need to fill out any extra forms or make some settings in the app?

The answer is no extra steps are needed.

The app you use for SIPs (or plan to use) already has an SWP option for most mutual funds—you just need to select it.

I know for a fact that top apps like Zerodha and Groww have this option.

I can't say with 100% certainty about other apps, but most of them should have it.

Setting up SWP is even easier than setting up SIP—you just need to go and select the option!

Who Should Invest in an SWP Plan?

The Systematic Withdrawal Plan (SWP) is a great investment option for individuals who need a regular cash flow while ensuring their capital keeps growing. Here’s who can benefit the most from it:

1. Retirees Looking for a Stable Income

Ideal for those who no longer have a fixed salary but need a steady monthly income.

Helps cover daily expenses without depleting savings.

2. Individuals with Financial Dependents

Suitable for people who have family members relying on them, such as children, elderly parents, or spouses.

Ensures a continuous flow of income to manage household expenses.

3. Investors Seeking Passive Income

Perfect for those who want to create an additional income stream while keeping their investments intact.

A great way to supplement earnings without actively managing investments.

4. Individuals Who Want to Beat Inflation

Bank FDs and traditional savings often fail to keep up with inflation.

SWP provides market-linked returns, helping your wealth grow over time.

5. People Who Want Tax-Efficient Withdrawals

Unlike fixed deposits, SWP offers lower tax liability due to long-term capital gains tax benefits.

No TDS (Tax Deducted at Source) on withdrawals.

6. Those Who Prefer Low-Risk, Disciplined Investing

SWP ensures regular withdrawals without panic-selling in volatile markets.

Eliminates the need to time the market, making it a stress-free investment option.

Best SWP Calculator

SWP stands for systematic withdrawal plan. If you invest a lump-sum amount in a mutual fund and you want to withdraw a certain amount regularly, then you can do the same with the help of SWP. And to calculate the total withdrawable amount, the final amount, and the amount invested, we use the SWP calculator.

Link - https://bekifaayati.co/pages/swp-calculator/

Factors to Consider Before Investing in SWP Funds

Strong Track Record – Choose funds with a consistent performance history for stable returns.

Low Fees – Opt for funds with a reasonable expense ratio to maximize profits.

Risk-Return Balance – Understand the risk level of the fund and match it with your financial goals.

Fund Type & Asset Allocation – Pick between equity, debt, or hybrid funds based on your risk appetite and withdrawal timeline.

Tax Efficiency – Be aware of capital gains tax on withdrawals to optimize returns.

Conclusion

SWP is a simple yet effective way to create a regular income stream while keeping your money invested for growth. It works well for retirees, individuals with dependents, or anyone looking for financial stability without relying on market timing.

The key to making the most of SWP is choosing the right fund, understanding withdrawal rates, and staying consistent with your investment approach. With proper planning, SWP can help you maintain cash flow, grow your wealth, and secure your financial future.

Subscribe to our newsletter

Unlock your financial potential with Zomint. We provide personalized tools and insights to elevate your financial journey.

Subscribe

to our newsletter

Unlock your financial potential with Zomint. We provide personalized tools and insights to elevate your financial journey.

Subscribe to our newsletter

Unlock your financial potential with Zomint. We provide personalized tools and insights to elevate your financial journey.