Zomint Blog

Tax Loss Harvesting: The Complete Playbook

Most investors know that good investing is about picking winners. Fewer realise that managing losers is just as important, and that a portfolio's under performers can be legally converted into a tax advantage worth lakhs every year.

For this March, our advisors at Zomint are checking each client's portfolio for unrealised losses sitting quietly alongside their gains. This isn't pessimism. It's tax loss harvesting, one of the most reliable, legal, and underused tools in wealth management.

Done right, it can save you tens of thousands of rupees in tax every year without changing your long-term investment thesis. Done wrong, or not done at all, you leave money on the table that the government is happy to collect.

This newsletter breaks down exactly how it works, what the FY 2026-27 rules look like, and the traps you must avoid.

FIRST, THE NUMBERS YOU NEED TO KNOW

Before we get into strategy, let's anchor on the current tax rules for FY 2026-27 under the New Tax Regime.

Tax Type | Holding Period | Rate | Key Exemption |

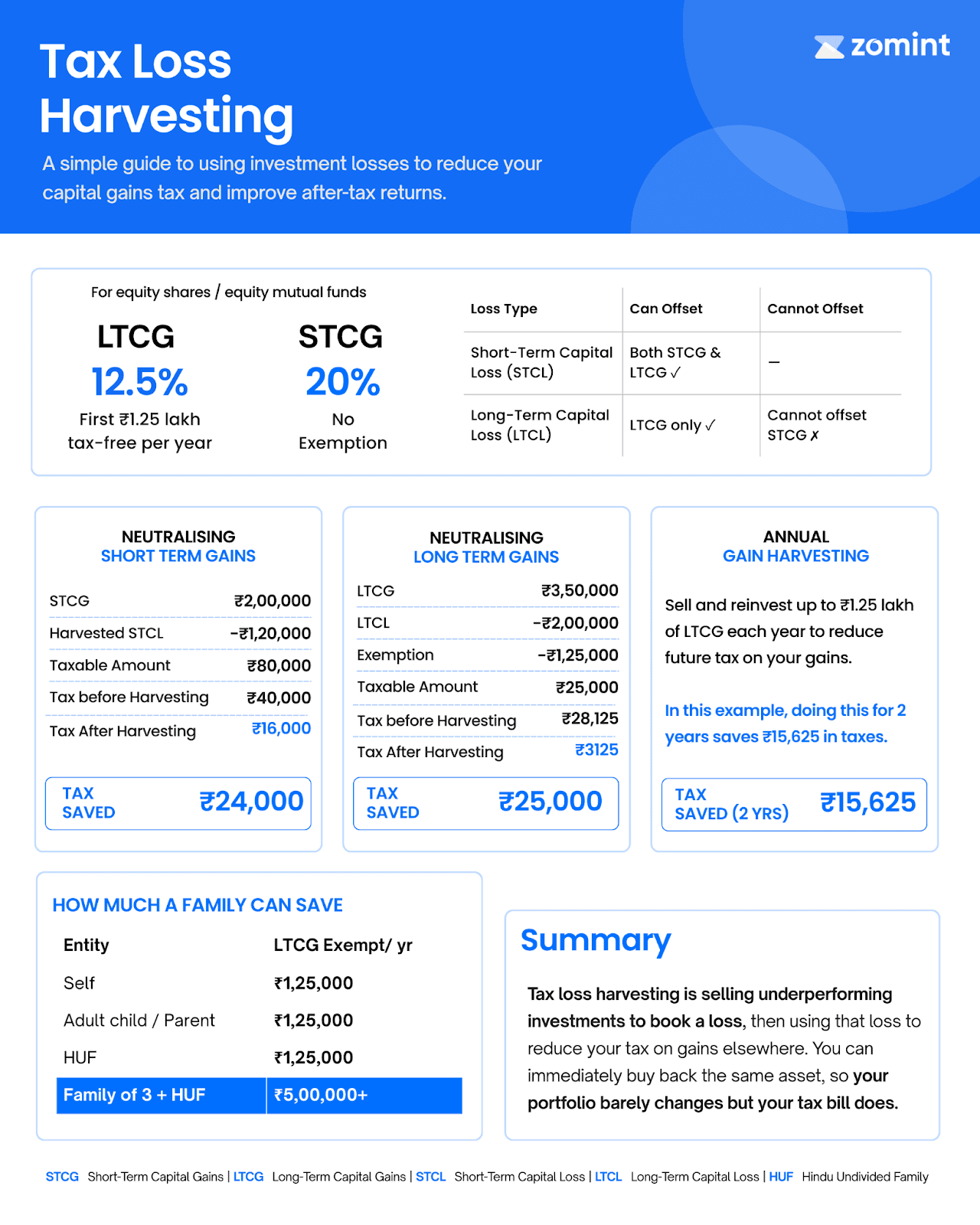

Long-Term Capital Gains (LTCG) on equity | More than 12 months | 12.5% | First Rs 1.25 lakh per year is tax free |

Short-Term Capital Gains (STCG) on equity | Less than 12 months | 20% | None. Every rupee is taxed. |

Section 87A Rebate | Not applicable | Up to Rs 60,000 | Zero tax on regular income if total regular income is up to Rs 12 lakh. Does not apply to capital gains from equity. |

Two things to know that are super critical for Tax Loss Harvesting.

First, the Rs 1.25 lakh LTCG exemption cannot be carried forward. If you don't use it in a financial year, it's gone forever.

Second, and this is where most people get confused: the Section 87A rebate does not apply to equity capital gains, not LTCG, not STCG. Even if your total income is below Rs 12 lakh, any equity capital gains above the Rs 1.25 lakh exemption will be taxed at their respective rates. The rebate only zeroes out your tax on regular slab-rate income. We will come back to this when we cover the traps.

WHAT IS TAX LOSS HARVESTING?

Tax loss harvesting is straightforward. You sell an investment that is currently trading below your purchase price, realise the loss on paper, and use that loss to offset the gains you have made elsewhere, reducing the amount of tax you owe.

Then, because India has no wash sale rule (more on this shortly), you can buy the same or a similar asset back the very next trading day. Your portfolio exposure barely changes. Your tax bill does.

There are two types of losses, and how you use them matters:

Loss Type | Can Offset | Cannot Offset | Carry Forward |

Short-Term Capital Loss (STCL) | Both STCG and LTCG | Nothing | Up to 8 assessment years |

Long-Term Capital Loss (LTCL) | LTCG only | STCG | Up to 8 assessment years |

The most valuable loss to harvest is STCL. It can knock out STCG that would otherwise be taxed at a steep 20%, making each rupee of STCL worth 20 paise in immediate tax savings.

STRATEGY IN ACTION

Scenario A: Neutralising Short-Term Gains

Imagine you booked a quick Rs 2,00,000 short-term gain earlier in the year. Maybe you exited a position after a sharp rally. You also hold a legacy tech stock that is down Rs 1,20,000 from your purchase price.

Here is what harvesting that tech stock loss does:

Without Harvesting | With Harvesting | |

Realised STCG | Rs 2,00,000 | Rs 2,00,000 |

Realised STCL (Harvested Loss) | Rs 0 | Rs 1,20,000 |

Net Taxable STCG | Rs 2,00,000 | Rs 80,000 |

Tax Payable at 20% | Rs 40,000 | Rs 16,000 |

Tax saved: Rs 24,000, by identifying and exiting one underperforming position.

Scenario B:Shielding Long-Term Gains

Now consider you are sitting on Rs 3,50,000 in long-term gains, well above the Rs 1.25 lakh exemption. You also hold an underperforming fund with Rs 2,00,000 in unrealised long-term losses.

Without Harvesting | With Harvesting | |

Realised LTCG | Rs 3,50,000 | Rs 3,50,000 |

Harvested LTCL | Rs 0 | Rs 2,00,000 |

Net LTCG | Rs 3,50,000 | Rs 1,50,000 |

Less: Annual Exemption | Rs 1,25,000 | Rs 1,25,000 |

Taxable LTCG | Rs 2,25,000 | Rs 25,000 |

Tax Payable at 12.5% | Rs 28,125 | Rs 3,125 |

Tax saved: Rs 25,000. Harvesting the loss brought the net gain almost entirely within the tax-free exemption limit.

Scenario C: GAIN HARVESTING

Most people focus only on losses. But capital gain harvesting is equally powerful and often overlooked.

The logic is simple. Because the Rs 1.25 lakh LTCG exemption is use-it-or-lose-it, you should deliberately realise up to Rs 1.25 lakh in long-term gains every year, even if you plan to hold the investment long-term. Selling and immediately reinvesting resets your cost base at a higher price. This means less taxable gain when you eventually sell for good.

Year 1 Action | Year 2 Action | Taxable LTCG | Tax at 12.5% | |

Without Harvesting | Hold | Sell all (Rs 3L gain) | Rs 3L minus Rs 1.25L = Rs 1.75L | Rs 21,875 |

With Gain Harvesting | Sell and reinvest Rs 1.25L gain | Sell all (Rs 1.75L gain) | Rs 1.75L minus Rs 1.25L = Rs 50,000 | Rs 6,250 |

Rs 15,625 can be saved in 2 years. Multiply this over 10 years and the compounding effect on your post-tax wealth becomes substantial.

THE TRAPS: WHERE INVESTORS GO WRONG

Trap 1: The Same-Day Buyback Mistake

This is the most common error we see. An investor sells a stock from their Demat account and buys it back the same day, expecting to harvest a loss. What actually happens: the broker treats this as an intraday trade.

The original delivery shares remain untouched in the Demat. No loss is harvested. Instead, the price difference is booked as Speculative Business Income, which is a completely different tax category.

Action | What You Think Happens | What Actually Happens |

Sell and buy same stock, same day | Capital loss harvested | No loss. Treated as intraday. Speculative income booked. |

Sell and buy same stock on T+1 (next trading day) | Capital loss harvested | Yes. Loss successfully booked. |

Sell from your Demat, buy in spouse's Demat same day | Capital loss harvested | Yes. Works. Continuous market exposure maintained. |

This trap applies to direct equity only. Mutual fund switches work differently. Each buy and sell triggers distinct NAVs, so same-day switching successfully harvests a gain or loss.

Trap 2: The Carry-Forward Ordering Trap

This one surprises even experienced investors. Under the Income Tax Act, if you have brought-forward losses from previous years, they must be set off against current year gains before the Rs 1.25 lakh exemption is applied. The exemption only applies to whatever net gain remains after the mandatory set-off.

Here is why this matters. Suppose you have Rs 1.5 lakh in brought-forward LTCL and you decide to harvest exactly Rs 1.25 lakh in gains this year, thinking the exemption will cover it:

Step | Calculation | Amount |

Current Year Gross LTCG | Deliberately harvested | Rs 1,25,000 |

Mandatory Set-Off (Brought-Forward LTCL) | IT Act requires this first | Rs 1,25,000 consumed |

Net LTCG before exemption | After compulsory loss adjustment | Rs 0 |

Rs 1.25L Annual Exemption Applied | To Rs 0 remaining | Rs 0. The entire limit was wasted. |

Remaining Carry-Forward Loss | Rs 1.5L minus Rs 1.25L consumed | Only Rs 25,000 left to carry forward |

Trap 3: The 87A Misconception

Capital gains are always taxed, even if your income is below Rs 12 lakh.

This is the trap that catches the most people, especially retail investors who have read that income up to Rs 12 lakh is tax-free under the new regime.

That is true for regular slab-rate income. It is not true for equity capital gains.

The Finance Act 2025 has expressly clarified this: the Section 87A rebate cannot be applied against income taxed at special rates. That includes both STCG under Section 111A (taxed at 20%) and LTCG under Section 112A (taxed at 12.5%). This applies from AY 2026-27 onwards with no ambiguity.

What this means in practice:

Scenario | Regular Income | LTCG Booked | Tax on Regular Income | Tax on Capital Gains | Net Tax |

No equity gains | Rs 10,00,000 | Rs 0 | Rs 0 (87A rebate covers it) | Rs 0 | Rs 0 |

Within exemption | Rs 10,00,000 | Rs 1,25,000 | Rs 0 (87A rebate) | Rs 0 (within Rs 1.25L limit) | Rs 0 |

Above exemption | Rs 10,00,000 | Rs 2,00,000 | Rs 0 (87A rebate) | Rs 9,375 (12.5% on Rs 75,000) | Rs 9,750 with cess |

High gains | Rs 10,00,000 | Rs 5,00,000 | Rs 0 (87A rebate) | Rs 46,875 (12.5% on Rs 3.75L) | Rs 48,750 with cess |

MULTIPLYING YOUR EXEMPTIONS: FAMILY STRUCTURING

The Rs 1.25 lakh LTCG exemption is per PAN, not per household. For investors sitting on large unrealised gains, the individual limit is often not enough. Here is how advisors legally multiply it.

Entity | Annual LTCG Exempt | Basic Exemption | Notes |

Individual (Self) | Rs 1,25,000 | Rs 4,00,000 | Standard. Every investor gets this. |

Adult Child (18 and above) or Retired Parent | Rs 1,25,000 | Rs 4,00,000 | Gifts to adult children or parents attract no clubbing provisions |

HUF (Hindu Undivided Family) | Rs 1,25,000 | Rs 4,00,000 | Separate PAN with completely independent limits |

Total: Family of 3 plus HUF | Rs 5,00,000 and above | Rs 16,00,000 and above | Combined exemption shield across four separate entities |

Critical note on the clubbing trap: Gifting assets to your spouse or minor children does not work.

Under Section 64 of the Income Tax Act, capital gains from assets gifted to a spouse or minor child are clubbed back into the donor's income. You achieve zero tax savings. Always gift to adult children (18 and above) or parents.

YOUR MARCH 2026 TAX HARVESTING CHECKLIST

Review your portfolio for all unrealised losses, both short-term and long-term.

Calculate your current year's net capital gains position across all realised transactions so far.

Check if you have brought-forward losses from previous years. These must be set off against current year gains before the Rs 1.25L exemption applies.

Model your full tax position before executing any trade. Understand your regular income and capital gains separately, since they are taxed independently and the 87A rebate only helps the former.

Execute gain harvesting if you have not already: sell and reinvest to realise up to Rs 1.25L in LTCG before March 31.

Execute loss harvesting: sell underperformers to offset taxable gains.

For direct equities: buy back on T+1 only. Never the same day.

For mutual funds: a switch is the cleanest execution method. It harvests the gain or loss without pulling money out of the market.

If you have adult family members or an HUF: explore whether assets can be structured across entities to multiply available exemptions.

Consult your advisor before acting. A single misstep, the wrong day of buyback, harvesting into carry-forward losses, or misunderstanding the 87A rules, can cost more than the tax you were trying to save.

CONCLUSION

Tax loss harvesting is not about chasing losses. It is about being intentional, recognising that every financial year has a March 31 deadline, after which that year's opportunities are gone permanently.

The difference between a well-managed portfolio and a passively-held one is not just returns. It is the post-tax returns that actually land in your hands. Over a decade, disciplined harvesting can meaningfully compound your real wealth, not just your notional gains.

If you would like us to review your portfolio for harvesting opportunities before March 31, reach out to your Zomint advisor. We are happy to help

Disclaimer: This newsletter is for educational and informational purposes only and does not constitute investment, tax, legal, or financial advice.

Most investors know that good investing is about picking winners. Fewer realise that managing losers is just as important, and that a portfolio's under performers can be legally converted into a tax advantage worth lakhs every year.

For this March, our advisors at Zomint are checking each client's portfolio for unrealised losses sitting quietly alongside their gains. This isn't pessimism. It's tax loss harvesting, one of the most reliable, legal, and underused tools in wealth management.

Done right, it can save you tens of thousands of rupees in tax every year without changing your long-term investment thesis. Done wrong, or not done at all, you leave money on the table that the government is happy to collect.

This newsletter breaks down exactly how it works, what the FY 2026-27 rules look like, and the traps you must avoid.

FIRST, THE NUMBERS YOU NEED TO KNOW

Before we get into strategy, let's anchor on the current tax rules for FY 2026-27 under the New Tax Regime.

Tax Type | Holding Period | Rate | Key Exemption |

Long-Term Capital Gains (LTCG) on equity | More than 12 months | 12.5% | First Rs 1.25 lakh per year is tax free |

Short-Term Capital Gains (STCG) on equity | Less than 12 months | 20% | None. Every rupee is taxed. |

Section 87A Rebate | Not applicable | Up to Rs 60,000 | Zero tax on regular income if total regular income is up to Rs 12 lakh. Does not apply to capital gains from equity. |

Two things to know that are super critical for Tax Loss Harvesting.

First, the Rs 1.25 lakh LTCG exemption cannot be carried forward. If you don't use it in a financial year, it's gone forever.

Second, and this is where most people get confused: the Section 87A rebate does not apply to equity capital gains, not LTCG, not STCG. Even if your total income is below Rs 12 lakh, any equity capital gains above the Rs 1.25 lakh exemption will be taxed at their respective rates. The rebate only zeroes out your tax on regular slab-rate income. We will come back to this when we cover the traps.

WHAT IS TAX LOSS HARVESTING?

Tax loss harvesting is straightforward. You sell an investment that is currently trading below your purchase price, realise the loss on paper, and use that loss to offset the gains you have made elsewhere, reducing the amount of tax you owe.

Then, because India has no wash sale rule (more on this shortly), you can buy the same or a similar asset back the very next trading day. Your portfolio exposure barely changes. Your tax bill does.

There are two types of losses, and how you use them matters:

Loss Type | Can Offset | Cannot Offset | Carry Forward |

Short-Term Capital Loss (STCL) | Both STCG and LTCG | Nothing | Up to 8 assessment years |

Long-Term Capital Loss (LTCL) | LTCG only | STCG | Up to 8 assessment years |

The most valuable loss to harvest is STCL. It can knock out STCG that would otherwise be taxed at a steep 20%, making each rupee of STCL worth 20 paise in immediate tax savings.

STRATEGY IN ACTION

Scenario A: Neutralising Short-Term Gains

Imagine you booked a quick Rs 2,00,000 short-term gain earlier in the year. Maybe you exited a position after a sharp rally. You also hold a legacy tech stock that is down Rs 1,20,000 from your purchase price.

Here is what harvesting that tech stock loss does:

Without Harvesting | With Harvesting | |

Realised STCG | Rs 2,00,000 | Rs 2,00,000 |

Realised STCL (Harvested Loss) | Rs 0 | Rs 1,20,000 |

Net Taxable STCG | Rs 2,00,000 | Rs 80,000 |

Tax Payable at 20% | Rs 40,000 | Rs 16,000 |

Tax saved: Rs 24,000, by identifying and exiting one underperforming position.

Scenario B:Shielding Long-Term Gains

Now consider you are sitting on Rs 3,50,000 in long-term gains, well above the Rs 1.25 lakh exemption. You also hold an underperforming fund with Rs 2,00,000 in unrealised long-term losses.

Without Harvesting | With Harvesting | |

Realised LTCG | Rs 3,50,000 | Rs 3,50,000 |

Harvested LTCL | Rs 0 | Rs 2,00,000 |

Net LTCG | Rs 3,50,000 | Rs 1,50,000 |

Less: Annual Exemption | Rs 1,25,000 | Rs 1,25,000 |

Taxable LTCG | Rs 2,25,000 | Rs 25,000 |

Tax Payable at 12.5% | Rs 28,125 | Rs 3,125 |

Tax saved: Rs 25,000. Harvesting the loss brought the net gain almost entirely within the tax-free exemption limit.

Scenario C: GAIN HARVESTING

Most people focus only on losses. But capital gain harvesting is equally powerful and often overlooked.

The logic is simple. Because the Rs 1.25 lakh LTCG exemption is use-it-or-lose-it, you should deliberately realise up to Rs 1.25 lakh in long-term gains every year, even if you plan to hold the investment long-term. Selling and immediately reinvesting resets your cost base at a higher price. This means less taxable gain when you eventually sell for good.

Year 1 Action | Year 2 Action | Taxable LTCG | Tax at 12.5% | |

Without Harvesting | Hold | Sell all (Rs 3L gain) | Rs 3L minus Rs 1.25L = Rs 1.75L | Rs 21,875 |

With Gain Harvesting | Sell and reinvest Rs 1.25L gain | Sell all (Rs 1.75L gain) | Rs 1.75L minus Rs 1.25L = Rs 50,000 | Rs 6,250 |

Rs 15,625 can be saved in 2 years. Multiply this over 10 years and the compounding effect on your post-tax wealth becomes substantial.

THE TRAPS: WHERE INVESTORS GO WRONG

Trap 1: The Same-Day Buyback Mistake

This is the most common error we see. An investor sells a stock from their Demat account and buys it back the same day, expecting to harvest a loss. What actually happens: the broker treats this as an intraday trade.

The original delivery shares remain untouched in the Demat. No loss is harvested. Instead, the price difference is booked as Speculative Business Income, which is a completely different tax category.

Action | What You Think Happens | What Actually Happens |

Sell and buy same stock, same day | Capital loss harvested | No loss. Treated as intraday. Speculative income booked. |

Sell and buy same stock on T+1 (next trading day) | Capital loss harvested | Yes. Loss successfully booked. |

Sell from your Demat, buy in spouse's Demat same day | Capital loss harvested | Yes. Works. Continuous market exposure maintained. |

This trap applies to direct equity only. Mutual fund switches work differently. Each buy and sell triggers distinct NAVs, so same-day switching successfully harvests a gain or loss.

Trap 2: The Carry-Forward Ordering Trap

This one surprises even experienced investors. Under the Income Tax Act, if you have brought-forward losses from previous years, they must be set off against current year gains before the Rs 1.25 lakh exemption is applied. The exemption only applies to whatever net gain remains after the mandatory set-off.

Here is why this matters. Suppose you have Rs 1.5 lakh in brought-forward LTCL and you decide to harvest exactly Rs 1.25 lakh in gains this year, thinking the exemption will cover it:

Step | Calculation | Amount |

Current Year Gross LTCG | Deliberately harvested | Rs 1,25,000 |

Mandatory Set-Off (Brought-Forward LTCL) | IT Act requires this first | Rs 1,25,000 consumed |

Net LTCG before exemption | After compulsory loss adjustment | Rs 0 |

Rs 1.25L Annual Exemption Applied | To Rs 0 remaining | Rs 0. The entire limit was wasted. |

Remaining Carry-Forward Loss | Rs 1.5L minus Rs 1.25L consumed | Only Rs 25,000 left to carry forward |

Trap 3: The 87A Misconception

Capital gains are always taxed, even if your income is below Rs 12 lakh.

This is the trap that catches the most people, especially retail investors who have read that income up to Rs 12 lakh is tax-free under the new regime.

That is true for regular slab-rate income. It is not true for equity capital gains.

The Finance Act 2025 has expressly clarified this: the Section 87A rebate cannot be applied against income taxed at special rates. That includes both STCG under Section 111A (taxed at 20%) and LTCG under Section 112A (taxed at 12.5%). This applies from AY 2026-27 onwards with no ambiguity.

What this means in practice:

Scenario | Regular Income | LTCG Booked | Tax on Regular Income | Tax on Capital Gains | Net Tax |

No equity gains | Rs 10,00,000 | Rs 0 | Rs 0 (87A rebate covers it) | Rs 0 | Rs 0 |

Within exemption | Rs 10,00,000 | Rs 1,25,000 | Rs 0 (87A rebate) | Rs 0 (within Rs 1.25L limit) | Rs 0 |

Above exemption | Rs 10,00,000 | Rs 2,00,000 | Rs 0 (87A rebate) | Rs 9,375 (12.5% on Rs 75,000) | Rs 9,750 with cess |

High gains | Rs 10,00,000 | Rs 5,00,000 | Rs 0 (87A rebate) | Rs 46,875 (12.5% on Rs 3.75L) | Rs 48,750 with cess |

MULTIPLYING YOUR EXEMPTIONS: FAMILY STRUCTURING

The Rs 1.25 lakh LTCG exemption is per PAN, not per household. For investors sitting on large unrealised gains, the individual limit is often not enough. Here is how advisors legally multiply it.

Entity | Annual LTCG Exempt | Basic Exemption | Notes |

Individual (Self) | Rs 1,25,000 | Rs 4,00,000 | Standard. Every investor gets this. |

Adult Child (18 and above) or Retired Parent | Rs 1,25,000 | Rs 4,00,000 | Gifts to adult children or parents attract no clubbing provisions |

HUF (Hindu Undivided Family) | Rs 1,25,000 | Rs 4,00,000 | Separate PAN with completely independent limits |

Total: Family of 3 plus HUF | Rs 5,00,000 and above | Rs 16,00,000 and above | Combined exemption shield across four separate entities |

Critical note on the clubbing trap: Gifting assets to your spouse or minor children does not work.

Under Section 64 of the Income Tax Act, capital gains from assets gifted to a spouse or minor child are clubbed back into the donor's income. You achieve zero tax savings. Always gift to adult children (18 and above) or parents.

YOUR MARCH 2026 TAX HARVESTING CHECKLIST

Review your portfolio for all unrealised losses, both short-term and long-term.

Calculate your current year's net capital gains position across all realised transactions so far.

Check if you have brought-forward losses from previous years. These must be set off against current year gains before the Rs 1.25L exemption applies.

Model your full tax position before executing any trade. Understand your regular income and capital gains separately, since they are taxed independently and the 87A rebate only helps the former.

Execute gain harvesting if you have not already: sell and reinvest to realise up to Rs 1.25L in LTCG before March 31.

Execute loss harvesting: sell underperformers to offset taxable gains.

For direct equities: buy back on T+1 only. Never the same day.

For mutual funds: a switch is the cleanest execution method. It harvests the gain or loss without pulling money out of the market.

If you have adult family members or an HUF: explore whether assets can be structured across entities to multiply available exemptions.

Consult your advisor before acting. A single misstep, the wrong day of buyback, harvesting into carry-forward losses, or misunderstanding the 87A rules, can cost more than the tax you were trying to save.

CONCLUSION

Tax loss harvesting is not about chasing losses. It is about being intentional, recognising that every financial year has a March 31 deadline, after which that year's opportunities are gone permanently.

The difference between a well-managed portfolio and a passively-held one is not just returns. It is the post-tax returns that actually land in your hands. Over a decade, disciplined harvesting can meaningfully compound your real wealth, not just your notional gains.

If you would like us to review your portfolio for harvesting opportunities before March 31, reach out to your Zomint advisor. We are happy to help

Disclaimer: This newsletter is for educational and informational purposes only and does not constitute investment, tax, legal, or financial advice.