India now has a regulated, goal‑linked mutual fund that automatically de-risks as your target date approaches. Here is what that means and why it matters.

Summary

SEBI has discontinued the solution‑oriented mutual funds category (retirement and children’s funds) and replaced it with Life Cycle Funds — a new category built around a fixed maturity year and a mandatory glide path.

The portfolio automatically shifts from equity to debt as the target date approaches, within SEBI‑defined allocation bands. No manual rebalancing is required.

The problem this solves

For decades, the most common mistake in Indian retail investing has not been choosing the wrong fund. It has been failing to adjust the portfolio when circumstances required it.

Investors who began SIPs in equity funds at 30 often continued holding the same equity‑heavy allocation at 55. Not necessarily by choice — but because rebalancing requires attention, discipline, and timing that many investors find difficult to maintain consistently.

As a result, portfolios often remained aggressive long after they should have gradually shifted toward stability.

Life Cycle Funds address this problem by embedding rebalancing directly into the product structure.

How it works

You select a fund tied to a specific target year — for example, 2045.

The fund begins with a higher allocation to equity for growth and then systematically shifts toward debt as the target year approaches.

This shift follows a predefined glide path, which automatically adjusts the asset allocation over time within SEBI‑prescribed ranges for equity, debt and other assets such as gold, silver, ETCDs (gold/silver only), and InvITs.

Investors therefore do not need to time the market or manually rebalance the portfolio.

This structure has a strong global precedent. In the United States, Target Date Funds manage roughly 5.2 trillion dollars in assets across mutual funds, CITs and custom solutions, and are the dominant default investment in 401(k) plans. Surveys show that around 87% of plans that use a qualified default investment alternative (QDIA) choose a target date fund as that default investment option.

India now has a regulated category that plays a similar role for goal‑based investing.

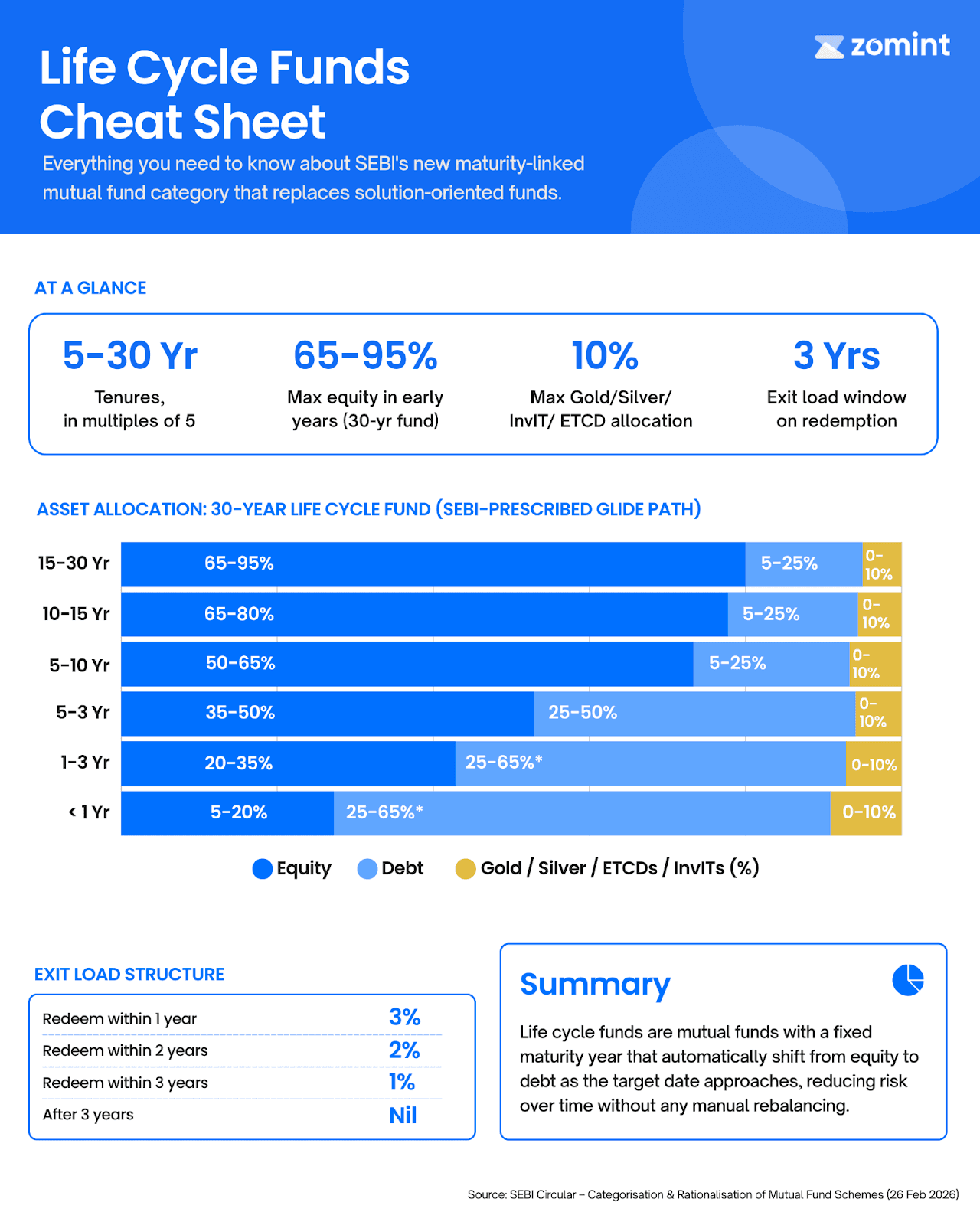

The SEBI glide path: Asset allocation, 30‑year fund

SEBI prescribes allocation bands, not fixed allocations.

When the fund has a long investment horizon, equity exposure can be as high as 95%. As the maturity date approaches, the permitted equity ceiling declines in stages. By the final year, equity exposure is capped at 5–20%, with debt carrying the majority of the portfolio.

Because SEBI defines ranges rather than fixed allocations, two funds with the same maturity year can still have meaningfully different portfolios. The way each fund house positions its portfolio within these bands will influence actual outcomes.

SEBI‑prescribed bands for a 30‑year Life Cycle Fund

Years to Maturity | Phase | Equity (%) | Debt (%) | Gold / Silver / ETCDs / InvITs (%) |

15 to 30 years | Aggressive | 65 to 95 | 5 to 25 | 0 to 10 |

10 to 15 years | Moderate | 65 to 80 | 5 to 25 | 0 to 10 |

5 to 10 years | Transition | 50 to 65 | 5 to 25 | 0 to 10 |

3 to 5 years | Conservative | 35 to 50 | 25 to 50 | 0 to 10 |

1 to 3 years | Very Conservative | 20 to 35 | 25 to 65* | 0 to 10 |

Less than 1 year | Highly Conservative | 5 to 20 | 25 to 65* | 0 to 10 |

*For schemes with 1 to 3 years remaining, debt investments must be restricted to AA and above rated instruments with residual maturity not exceeding the target maturity.

SEBI also permits funds with less than five years to maturity to use equity arbitrage (up to 50% of the portfolio) in addition to the glide‑path equity range, provided total equity and equity‑related exposure stays between 65% and 75%. This may vary by scheme but does not change the broad allocation bands.

Source: SEBI circular on Categorization and Rationalization of Mutual Fund Schemes, February 26, 2026.

Exit load structure

Life Cycle Funds are open‑ended and do not have a mandatory lock‑in period. Investors can redeem their units at any time.

However, the exit load structure is designed to encourage long‑term holding aligned with the fund’s tenure:

Redemption Time | Exit Load |

Redeem within 1 year | 3% |

Redeem within 2 years | 2% |

Redeem within 3 years | 1% |

After 3 years | Nil |

What to keep in mind

Life Cycle Funds can work well for investors who want a single, self‑managing product aligned with a specific goal year. The built‑in structure reduces the need for constant intervention, which can be genuinely helpful.

However, a few considerations remain important before investing:

Glide path vs. entry date

The glide path runs based on the fund’s launch date, not your entry date. Entering a 2045 fund in 2040 means buying into a portfolio that may already be relatively conservative, leaving limited time for equity‑driven growth.

Match maturity to the goal

Match the maturity year to your goal, not to your age. A Life Cycle Fund maturing in 2050 may not be suitable for a financial goal that requires funds in 2040.

Evaluate the glide path strategy

SEBI sets the boundaries, but how a fund house manages allocations within those bands — equity level in each bucket, use of arbitrage, debt quality, and gold/silver exposure — will affect performance and risk.

Expense ratios matter

Expense ratios matter significantly over long horizons. Even a 0.5 percentage point annual difference can compound into a meaningful drag over a 20–30 year investment period.

Complex goals still need advice

For investors with more complex goals, varying timelines, or evolving risk profiles, a structured advisory relationship with periodic portfolio rebalancing can offer greater flexibility.

Life Cycle Funds are a useful tool. They are not a substitute for a comprehensive financial plan.

Solution‑Oriented Funds (Discontinued) vs Life Cycle Funds (New)

Feature | Solution‑Oriented Funds (Discontinued) | Life Cycle Funds (New) |

Label / positioning | Goal‑labelled (retirement / children) | Maturity year embedded in scheme name (for example, Life Cycle Fund 2045) |

Target date | No fixed target date; broad long‑term horizon | Fixed target date structure |

Glide path | No mandatory glide path; asset allocation changes were at the fund manager’s discretion | SEBI‑prescribed glide path with defined allocation bands over time |

Rebalancing | Manual rebalancing required by the investor or adviser | Automatic equity‑to‑debt shift over time within SEBI’s bands |

Lock‑in / liquidity | Open‑ended with mandatory 5‑year lock‑in (or till retirement / child’s majority); additional exit loads on units not under lock‑in | Open‑ended with no regulatory lock‑in; graded exit load of 3% / 2% / 1% within 3 years, Nil thereafter |

Regulatory status | Category discontinued by SEBI; existing schemes to be merged or reclassified | Active category; new launches expected across tenures from 5 to 30 years |

Who is this for?

Anyone with a clearly defined financial goal and a timeline of 5 to 30 years should understand this category.

Life Cycle Funds represent a structurally sound approach to goal‑based investing. Whether they are the right fit depends on:

Your specific goal and its timing.

The maturity year you choose.

The fund house’s glide path decisions within SEBI’s bands.

How the fund integrates with the rest of your portfolio and tax situation.

Disclaimer

Mutual fund investments are subject to market risks. Please read all scheme‑related documents carefully before investing. This content is for educational purposes only and does not constitute investment advice.

India now has a regulated, goal‑linked mutual fund that automatically de-risks as your target date approaches. Here is what that means and why it matters.

Summary

SEBI has discontinued the solution‑oriented mutual funds category (retirement and children’s funds) and replaced it with Life Cycle Funds — a new category built around a fixed maturity year and a mandatory glide path.

The portfolio automatically shifts from equity to debt as the target date approaches, within SEBI‑defined allocation bands. No manual rebalancing is required.

The problem this solves

For decades, the most common mistake in Indian retail investing has not been choosing the wrong fund. It has been failing to adjust the portfolio when circumstances required it.

Investors who began SIPs in equity funds at 30 often continued holding the same equity‑heavy allocation at 55. Not necessarily by choice — but because rebalancing requires attention, discipline, and timing that many investors find difficult to maintain consistently.

As a result, portfolios often remained aggressive long after they should have gradually shifted toward stability.

Life Cycle Funds address this problem by embedding rebalancing directly into the product structure.

How it works

You select a fund tied to a specific target year — for example, 2045.

The fund begins with a higher allocation to equity for growth and then systematically shifts toward debt as the target year approaches.

This shift follows a predefined glide path, which automatically adjusts the asset allocation over time within SEBI‑prescribed ranges for equity, debt and other assets such as gold, silver, ETCDs (gold/silver only), and InvITs.

Investors therefore do not need to time the market or manually rebalance the portfolio.

This structure has a strong global precedent. In the United States, Target Date Funds manage roughly 5.2 trillion dollars in assets across mutual funds, CITs and custom solutions, and are the dominant default investment in 401(k) plans. Surveys show that around 87% of plans that use a qualified default investment alternative (QDIA) choose a target date fund as that default investment option.

India now has a regulated category that plays a similar role for goal‑based investing.

The SEBI glide path: Asset allocation, 30‑year fund

SEBI prescribes allocation bands, not fixed allocations.

When the fund has a long investment horizon, equity exposure can be as high as 95%. As the maturity date approaches, the permitted equity ceiling declines in stages. By the final year, equity exposure is capped at 5–20%, with debt carrying the majority of the portfolio.

Because SEBI defines ranges rather than fixed allocations, two funds with the same maturity year can still have meaningfully different portfolios. The way each fund house positions its portfolio within these bands will influence actual outcomes.

SEBI‑prescribed bands for a 30‑year Life Cycle Fund

Years to Maturity | Phase | Equity (%) | Debt (%) | Gold / Silver / ETCDs / InvITs (%) |

15 to 30 years | Aggressive | 65 to 95 | 5 to 25 | 0 to 10 |

10 to 15 years | Moderate | 65 to 80 | 5 to 25 | 0 to 10 |

5 to 10 years | Transition | 50 to 65 | 5 to 25 | 0 to 10 |

3 to 5 years | Conservative | 35 to 50 | 25 to 50 | 0 to 10 |

1 to 3 years | Very Conservative | 20 to 35 | 25 to 65* | 0 to 10 |

Less than 1 year | Highly Conservative | 5 to 20 | 25 to 65* | 0 to 10 |

*For schemes with 1 to 3 years remaining, debt investments must be restricted to AA and above rated instruments with residual maturity not exceeding the target maturity.

SEBI also permits funds with less than five years to maturity to use equity arbitrage (up to 50% of the portfolio) in addition to the glide‑path equity range, provided total equity and equity‑related exposure stays between 65% and 75%. This may vary by scheme but does not change the broad allocation bands.

Source: SEBI circular on Categorization and Rationalization of Mutual Fund Schemes, February 26, 2026.

Exit load structure

Life Cycle Funds are open‑ended and do not have a mandatory lock‑in period. Investors can redeem their units at any time.

However, the exit load structure is designed to encourage long‑term holding aligned with the fund’s tenure:

Redemption Time | Exit Load |

Redeem within 1 year | 3% |

Redeem within 2 years | 2% |

Redeem within 3 years | 1% |

After 3 years | Nil |

What to keep in mind

Life Cycle Funds can work well for investors who want a single, self‑managing product aligned with a specific goal year. The built‑in structure reduces the need for constant intervention, which can be genuinely helpful.

However, a few considerations remain important before investing:

Glide path vs. entry date

The glide path runs based on the fund’s launch date, not your entry date. Entering a 2045 fund in 2040 means buying into a portfolio that may already be relatively conservative, leaving limited time for equity‑driven growth.

Match maturity to the goal

Match the maturity year to your goal, not to your age. A Life Cycle Fund maturing in 2050 may not be suitable for a financial goal that requires funds in 2040.

Evaluate the glide path strategy

SEBI sets the boundaries, but how a fund house manages allocations within those bands — equity level in each bucket, use of arbitrage, debt quality, and gold/silver exposure — will affect performance and risk.

Expense ratios matter

Expense ratios matter significantly over long horizons. Even a 0.5 percentage point annual difference can compound into a meaningful drag over a 20–30 year investment period.

Complex goals still need advice

For investors with more complex goals, varying timelines, or evolving risk profiles, a structured advisory relationship with periodic portfolio rebalancing can offer greater flexibility.

Life Cycle Funds are a useful tool. They are not a substitute for a comprehensive financial plan.

Solution‑Oriented Funds (Discontinued) vs Life Cycle Funds (New)

Feature | Solution‑Oriented Funds (Discontinued) | Life Cycle Funds (New) |

Label / positioning | Goal‑labelled (retirement / children) | Maturity year embedded in scheme name (for example, Life Cycle Fund 2045) |

Target date | No fixed target date; broad long‑term horizon | Fixed target date structure |

Glide path | No mandatory glide path; asset allocation changes were at the fund manager’s discretion | SEBI‑prescribed glide path with defined allocation bands over time |

Rebalancing | Manual rebalancing required by the investor or adviser | Automatic equity‑to‑debt shift over time within SEBI’s bands |

Lock‑in / liquidity | Open‑ended with mandatory 5‑year lock‑in (or till retirement / child’s majority); additional exit loads on units not under lock‑in | Open‑ended with no regulatory lock‑in; graded exit load of 3% / 2% / 1% within 3 years, Nil thereafter |

Regulatory status | Category discontinued by SEBI; existing schemes to be merged or reclassified | Active category; new launches expected across tenures from 5 to 30 years |

Who is this for?

Anyone with a clearly defined financial goal and a timeline of 5 to 30 years should understand this category.

Life Cycle Funds represent a structurally sound approach to goal‑based investing. Whether they are the right fit depends on:

Your specific goal and its timing.

The maturity year you choose.

The fund house’s glide path decisions within SEBI’s bands.

How the fund integrates with the rest of your portfolio and tax situation.

Disclaimer

Mutual fund investments are subject to market risks. Please read all scheme‑related documents carefully before investing. This content is for educational purposes only and does not constitute investment advice.